THE AI COMMAND

LEARNING MODULE

TAIC-LM-G04

Australian Securities and Investments Commission Act 2001 (Cth)

Consumer Protection in Financial Services

From misleading conduct prohibitions to AI-assisted marketing and PDS review

Executive Summary

The Australian Securities and Investments Commission Act 2001 (Cth) (the ASIC Act) sets the consumer protection floor for financial services in Australia. Division 2 of Part 2 of the Act prohibits misleading or deceptive conduct (s12DA), specific false or misleading representations (s12DB), unconscionable conduct in connection with financial services (s12CA, s12CB, s12CC), and unfair terms in standard form consumer and small business contracts (s12BF to s12BM). The prohibitions operate alongside the equivalent provisions of the Australian Consumer Law (ACL), the Corporations Act 2001 (Cth), and the Design and Distribution Obligations regime, and they are enforced by ASIC.

Why this matters

Consumer protection breaches are one of the largest sources of regulator action and remediation spend in Australian financial services. Penalty exposure for misleading conduct in a financial services context can run into hundreds of millions of dollars per matter, and the 2022 strengthening of the unfair contract terms regime introduced civil penalties for proposing, applying, or relying on an unfair term, on top of voiding the term. Marketing collateral, product disclosure statements, advertising, social media content, onboarding scripts, and standard form agreements all sit within the perimeter. Boards and Senior Managers carry accountability under the Financial Accountability Regime (FAR) for the design and operation of consumer protection controls, and ASIC has signalled that misleading conduct, predatory product design, and unfair terms are ongoing enforcement priorities.

What you will be able to do

1. Read Division 2 of Part 2 of the ASIC Act and identify which prohibitions apply to a given product, channel, or contract.

2. Run a structured red team review of a draft Product Disclosure Statement, brochure, or marketing campaign against s12DA and s12DB.

3. Decompose a transaction or contract against the statutory unconscionable conduct factors in s12CC.

4. Determine whether a contract falls within the unfair contract terms regime and assess each term against the s12BG test.

5. Stand up a governed AI-assisted marketing and PDS review workflow in Claude or ChatGPT that does not leak customer data and preserves a defensible audit trail.

Regulatory and Strategic Context

Issuer and statutory authority

The ASIC Act 2001 (Cth) is an Act of the Commonwealth Parliament. It establishes the Australian Securities and Investments Commission and confers on it the powers to administer the corporate, markets, financial services, and consumer credit law. Division 2 of Part 2 of the Act (sections 12AA to 12HD) sits within Part 2 (Unconscionable conduct and consumer protection in relation to financial services) and is the operative consumer protection chapter for the financial sector. The prohibitions are civil in character but several attract criminal liability under s12GB. ASIC has broad investigative powers under Part 3 of the Act, including notices to produce, examination powers, and the ability to commence civil penalty proceedings in the Federal Court.

Scope of application

The Division applies to conduct in trade or commerce in relation to financial services within the meaning of section 12BAB. A financial service is broadly defined and captures dealing in a financial product, providing financial product advice, making a market, providing custodial or depository services, providing traditional trustee services, and operating a registered managed investment scheme. The Division reaches authorised representatives, intermediaries, and product issuers; it is not limited to Australian Financial Services Licence (AFSL) holders. The geographical reach extends to conduct outside Australia by Australian residents and bodies corporate carrying on business in Australia under section 12AC, mirroring the extra-territorial reach of the Corporations Act.

Key dates and transitional periods

The ASIC Act commenced on 15 July 2001 (replacing the Australian Securities and Investments Commission Act 1989 (Cth)). The unfair contract terms regime in sections 12BF to 12BM was extended to small business contracts on 12 November 2016. The most material recent change is the Treasury Laws Amendment (More Competition, Better Prices) Act 2022 (Cth), which from 9 November 2023 introduced civil penalties for proposing, applying, or relying on an unfair contract term, expanded the small business definition (now businesses with fewer than 100 employees or annual turnover under $10 million), and removed the prior contract value cap. Successive Treasury and ASIC consultation papers in 2024 and 2025 have continued to reshape unconscionable conduct enforcement following the High Court decision in Productivity Partners Pty Ltd v ACCC [2024] HCA 27 (a Competition and Consumer Act case with read-across to s12CB).

Interplay with adjacent frameworks

Three adjacent frameworks must be operated in parallel. First, the Australian Consumer Law (ACL) in Schedule 2 to the Competition and Consumer Act 2010 (Cth) contains mirror provisions for non-financial services: section 18 (misleading or deceptive conduct), sections 20, 21, and 22 (unconscionable conduct), and sections 23 to 28 (unfair contract terms). Where a product or marketing piece spans both financial and non-financial services (for example, a bundled offer with a credit card and a retail rewards programme), both regimes apply and ASIC and the Australian Competition and Consumer Commission (ACCC) coordinate. Second, the Corporations Act 2001 (Cth) contains its own misleading conduct prohibition for financial products in section 1041H, which operates in addition to s12DA of the ASIC Act and is enforced by ASIC. Disclosure obligations under Part 7.9 of the Corporations Act (PDS regime) are the substantive disclosure standard against which misleading conduct is often measured. Third, the Design and Distribution Obligations (DDO) regime in Part 7.8A of the Corporations Act (Target Market Determinations) interlocks with consumer protection: a product distributed outside its target market will frequently raise both s12DA and DDO issues. Cross-references in this learning library include TAIC-LM-G01 (Corporations Act 2001), TAIC-LM-G02 (Privacy Act 1988 and APPs), and TAIC-LM-G03 (AML/CTF Act 2006).

In practice, consumer protection sits at the intersection of Marketing, Product, Legal, Compliance, and Distribution. The largest enforcement outcomes have arisen where these functions were poorly integrated and where a marketing claim or a contract term was approved without a structured consumer protection challenge.

Visual 1: Regulatory authority and jurisdiction map

Specification for a top-down jurisdictional flowchart suitable for Lucidchart or Whimsical render. Eight nodes, three layers, vertical orientation.

Core Concepts and Defined Terms

Defined terms

Central obligations

Misleading or deceptive conduct (s12DA)

Section 12DA imports a no-fault, objective test. Three elements must be made out: conduct in trade or commerce; in relation to financial services; that is misleading or deceptive or likely to mislead or deceive. Silence can be conduct where there is a reasonable expectation of disclosure. Future representations are caught and the burden under s12BB shifts to the maker to show reasonable grounds. Disclaimers can be effective only if sufficiently prominent and clear, and they cannot rescue conduct that is fundamentally misleading.

Specific false or misleading representations (s12DB)

Section 12DB lists ten enumerated representations, paragraphs (1)(a) to (1)(j), that are prohibited if false or misleading. Each paragraph is a discrete cause of action and attracts its own civil penalty exposure. The categories most often engaged in financial services are paragraphs (1)(a) (services of a particular standard, quality, value, or grade), (1)(e) (sponsorship, approval, performance characteristics, uses, or benefits), (1)(g) (the price of services), (1)(h) (the need for any services), and (1)(i) (the existence, exclusion, or effect of any condition, warranty, guarantee, right, or remedy).

Unconscionable conduct (s12CA, s12CB, s12CC)

Section 12CA prohibits conduct unconscionable within the meaning of the unwritten law (the equitable doctrine). Section 12CB prohibits statutory unconscionable conduct, which is broader and does not require proof of special disadvantage. Section 12CC sets out twelve non-exhaustive factors a court may consider, including the relative bargaining strength of the parties, whether the customer was required to comply with conditions not reasonably necessary, ability to understand documents, undue influence or unfair tactics, the amount and circumstances of comparable contracts, willingness to negotiate, the extent to which both parties acted in good faith, and risk allocation. Productivity Partners (HCA 2024) confirms statutory unconscionability does not require predatory motive but does require conduct departing significantly from norms of acceptable commercial behaviour.

Unfair contract terms (s12BF to s12BM)

The unfair contract terms regime applies to standard form consumer and small business contracts for financial services or financial products. A term is unfair under s12BG if it (1) causes a significant imbalance in the parties' rights and obligations, (2) is not reasonably necessary to protect a legitimate interest of the party advantaged by the term, and (3) would cause detriment (financial or otherwise) if relied on. Section 12BH lists examples of potentially unfair terms, including unilateral variation rights, unilateral termination rights, and limitations on the consumer's vicarious liability for agents. From 9 November 2023 a court may impose a civil penalty for proposing, applying, or relying on an unfair term, in addition to declaring the term void.

Visual 2: Misleading conduct enforcement lifecycle (process diagram)

Specification for a horizontal process diagram, eight stages, render as Mermaid for the designer.

flowchart LR

A[Conduct in trade or commerce] --> B[Marketing, PDS, advertising, statement, or contract term]

B --> C{Likely to mislead the relevant class of consumers?}

C -- No --> D[Document the consumer protection sign-off and retain artefacts]

C -- Yes --> E[Internal escalation: Legal, Compliance, Marketing approver]

E --> F[Customer remediation triggered, conduct corrected, retraction issued]

F --> G[Self-report to ASIC under s912D Corporations Act if reportable situation]

G --> H[ASIC investigation, civil penalty proceeding, or infringement notice]

Designer note: render as horizontal swimlanes mapped to Marketing, Legal/Compliance, Operations, and Regulator. Annotate decision points C and G with the controlling provisions (s12DA / s12DB and s912D).

Practical Application in Australian Financial Services

Before any pack like the four above reaches a customer, run it through a structured red team pass. The prompt below is copy-paste ready for a governed Claude or ChatGPT project space.

The next four worked examples translate the prohibitions into operational artefacts. Each uses de-identified scenarios with merge field placeholders. No real customer data.

Example 1: Authorised Deposit-taking Institution (ADI)

Trigger event: An ADI runs a marketing campaign promoting a new high-yield savings account. The headline claim is [HEADLINE_CLAIM] (for example, "5.00% p.a. introductory rate"). The footnoted disclosures explain that the rate applies only for the first four months, only to the first $50,000 of balance, and only where a paired transaction account meets monthly deposit thresholds. A subset of customers open the account expecting the headline rate to persist.

Obligation activated: section 12DA (overall impression of the campaign), section 12DB(1)(e) (representation that the services have performance characteristics, uses, or benefits, which captures the headline rate), section 12DB(1)(i) (existence, exclusion, or effect of conditions attached to the rate), and the Corporations Act s1041H mirror. Reportable situation analysis under s912D arises if the conduct amounts to a contravention of the financial services laws.

Artefact produced: a remediated marketing pack with prominently disclosed conditions on the same screen as the headline rate, an internal misleading conduct review memorandum, a customer remediation plan with a population estimate, and a draft self-report to ASIC for senior manager approval. A 12-month look-back across past campaigns is initiated.

Audit trail expected: marketing approval workflow showing Legal and Compliance sign-off with version history, the consumer protection red team checklist, the customer remediation register, the self-report submission receipt, and a control linkage to FAR-accountable Senior Managers.

Example 2: General insurer

Trigger event: A general insurer issues a home and contents Product Disclosure Statement (PDS) and supporting brochure. The brochure describes the policy as providing [COVER_TYPE] (for example, "comprehensive flood and storm cover"). The PDS contains a definition of flood that excludes certain riverine inundation events common in the customer's postcode.

Obligation activated: section 12DA, section 12DB(1)(a) (standard, quality, value, grade), section 12DB(1)(e) (performance characteristics, uses, or benefits of the cover), section 12DB(1)(i) (existence, exclusion, or effect of any condition), Insurance Contracts Act 1984 (Cth) duty of utmost good faith, and DDO Target Market Determination obligations under Part 7.8A of the Corporations Act.

Artefact produced: a PDS update with a plain English flood definition aligned to the Standard Definition of Flood under the Insurance Contracts Regulations, a campaign retraction, a customer communication explaining the change, and a remediation analysis identifying customers who may have been induced to purchase. The DDO TMD is reviewed for alignment.

Audit trail expected: PDS version control, the consumer protection sign-off log, a remediation register with payment status, the regulator notification (if reportable), and updated DDO governance minutes.

Example 3: Superannuation trustee

Trigger event: A superannuation trustee publishes investment performance data for the [PRODUCT_NAME] MySuper investment option. The performance figure is calculated on a basis that differs from the APRA Heatmap methodology and the difference is not prominently disclosed. Comparator marketing claims rank the option above peer offerings.

Obligation activated: section 12DA (overall impression and silence about a material methodological difference), section 12DB(1)(e) (performance characteristics, uses, or benefits), Corporations Act s1041H, and trustee best financial interests duty under s52(2)(c) of the SIS Act 1993 (Cth).

Artefact produced: revised performance disclosure aligned to the APRA Heatmap methodology, a comparator advertising sweep, a member communication explaining the change without alarming language, and a self-report assessment under s912D. The trustee's marketing approval procedures are amended to require explicit methodology declarations.

Audit trail expected: methodology working papers, marketing approval log, a member communications register, the s912D self-assessment file, and Board sub-committee minutes recording acceptance of the remediation plan.

Example 4: AFSL holder (managed investment scheme operator)

Trigger event: An AFSL-holding responsible entity offers a wholesale unit trust to small business clients. The application form is a standard form contract that includes a unilateral variation clause permitting the responsible entity to amend fees on 30 days' notice and an indemnity clause extending to losses arising from the responsible entity's own gross negligence.

Obligation activated: unfair contract terms regime under s12BF to s12BM (small business contract test satisfied), s12BG unfairness test (significant imbalance, not reasonably necessary, detriment), s12BH(1) examples of unfair terms (unilateral variation), statutory unconscionable conduct under s12CB, and AFSL general obligations under s912A of the Corporations Act.

Artefact produced: an amended standard form contract removing or rebalancing the impugned terms, an advice to existing customers, a refund or credit programme where reliance has occurred, and a control upgrade adding a standing UCT review at every contract revision. A compliance attestation is filed.

Audit trail expected: contract version control with redlines showing the change, an unfair contract term register, a customer impact analysis, the s912D self-report file (if applicable), and the Board risk committee resolution endorsing the standing review process.

Visual Pack (continued)

Visuals 3 to 8 below complete the inline visual pack and are designer-ready specifications for Lucidchart, Whimsical, or Figma without further interpretation.

Visual 3: Comparative table (s12DA ASIC Act vs s18 ACL vs s1041H Corporations Act)

Visual 4: RACI for marketing and PDS consumer protection sign-off

RACI key: R = Responsible, A = Accountable, C = Consulted, I = Informed.

Visual 5: Unconscionable conduct factors checklist and heat map (s12CC)

Specification for a 12-row heat map with three columns: factor (s12CC reference), risk likelihood (High, Medium, Low), and risk impact (High, Medium, Low). Designer should render likelihood and impact as filled coloured cells (red for High, amber for Medium, green for Low).

Designer note: render as a 12 by 2 matrix with each cell colour-coded. Add a left-side legend explaining likelihood and impact thresholds in plain English.

Visual 6: Unfair contract terms decision tree

Specification for a decision tree, single entry point, four terminal states. Render as Mermaid for the designer.

flowchart TD

A[Term in a contract for financial services or financial products] --> B{Standard form contract under s12BK?}

B -- No --> C[Outside the UCT regime. Other prohibitions still apply.]

B -- Yes --> D{Consumer (s12BF(3)) or small business (s12BF(4))?}

D -- No --> C

D -- Yes --> E{Term defines main subject matter, sets upfront price, or is required by law (s12BI)?}

E -- Yes --> C

E -- No --> F{Three-limb test under s12BG: significant imbalance + not reasonably necessary + detriment if relied on?}

F -- No --> G[Term valid. Document the assessment and retain evidence.]

F -- Yes --> H[Term unfair and void. Civil penalty exposure under post-2023 regime. Remediate, notify, and reissue contract.]

Visual 7: ASIC consumer protection enforcement outcomes (illustrative)

Specification for a bar and line combination chart. X axis: financial year (FY22 to FY26). Y axis (left): count of ASIC enforcement actions citing s12DA, s12DB, s12CB, or UCT contraventions. Y axis (right): aggregate civil penalty exposure ($m, illustrative). All figures must be labelled "illustrative" in the rendered visual.

Numbers in this table are illustrative only. They are not drawn from ASIC enforcement data and must not be cited as authoritative.

Visual 8: The five things to remember

Operating ASIC Act Consumer Protection With AI

The unfair contract terms scan is the highest leverage use case in this list, because every template in the contract register needs a documented s12BG assessment under the post-2023 penalty regime. Use this prompt as the first pass.

This section explains how to run a consumer protection workflow day to day with large language model support (Claude or ChatGPT, Enterprise tier). The workflow centres on screening marketing collateral, Product Disclosure Statements, brochures, advertising scripts, and standard form contracts for misleading conduct, unconscionable conduct, and unfair contract term risk. Reputation exposure on AI-generated marketing copy is high, so legal sign-off remains the gating step.

Use cases at scale

1. Misleading conduct red team review of a draft PDS, brochure, or campaign across the s12DB enumerated categories.

2. Unfair contract terms scan of a standard form agreement against the s12BG three-limb test and the s12BH examples.

3. Statutory unconscionable conduct risk register entries for product designs targeted at vulnerable or low-financial-literacy cohorts.

4. Plain English rewrite of disclosure paragraphs measured against the Flesch reading ease band appropriate for the target market.

5. Comparison of competing marketing claims across peers to identify implied superiority claims that would not survive challenge.

6. Drafting a customer remediation explanation letter that satisfies disclosure obligations without creating new misleading impressions.

7. Producing a Board paper executive summary on consumer protection exposure across business lines.

8. Triage of incoming ASIC information requests under s33 of the Act, structured for legal review.

Project space setup

Claude Project

Step 1. In Claude.ai, create a Project "ASIC Consumer Protection Workspace" on Enterprise or Team tier. Step 2. Upload knowledge sources: ASIC Act 2001 (Cth) Division 2 of Part 2, ASIC Regulatory Guides RG 234 (Advertising financial products), RG 168 (Disclosure: Product Disclosure Statements), RG 78 (Breach reporting by AFS licensees), Information Sheet 211 (Clear, concise and effective disclosure obligations), the entity's marketing approval policy, and the entity's standard form contract templates. Step 3. Set the system prompt: "You are a consumer protection compliance analyst for an Australian financial services entity. You operate under the ASIC Act 2001 (Cth), the Corporations Act 2001 (Cth), the Australian Consumer Law where relevant, and ASIC regulatory guidance. You never reproduce real customer or counterparty identifiers. You always cite the section, regulatory guide, or information sheet supporting your conclusion. You always flag the limits of your output: this is a draft for legal sign-off, not a legal opinion." Step 4. Naming: TAIC-{entity}-{type}-{YYYYMMDD}-{version}. Step 5. Configure Skills for the recurring tasks: "misleading-conduct-review", "uct-scan", "unconscionability-checklist", and "customer-remediation-letter".

ChatGPT Project or Custom GPT

Step 1. Create a Project (Plus, Team, or Enterprise) "ASIC Consumer Protection Workspace". Step 2. Upload the same knowledge sources. Step 3. Apply the same system prompt scaffold. Step 4. For Custom GPT, set Capabilities to file search only and disable web browsing on sensitive workflows. Step 5. On Enterprise, confirm no-training at workspace level and identity-provider integration with Microsoft 365 or Google Workspace. Step 6. Naming convention is identical.

Prompt library

Prompt 1: Misleading conduct red team review of a draft PDS

Role: ASIC Act consumer protection reviewer acting as red team. Context: an Australian {{ENTITY_TYPE}} has produced draft PDS for {{PRODUCT}}. Task: assess the PDS against s12DA and each paragraph of s12DB(1). Constraints: cite the relevant paragraph. No customer identifiers. Output Format: a table with columns Page or paragraph, Statement, Risk type, Subsection cited, Suggested remediation, Severity (High, Medium, Low). Quality Bar: every entry must reference a specific passage. Severity must be justified in one sentence. Mark the output DRAFT FOR LEGAL REVIEW.

Prompt 2: Unfair contract terms scan

Role: UCT analyst. Context: {{CONTRACT_NAME}} is a standard form contract for {{CONSUMER_OR_SMALL_BUSINESS}} customers. Task: assess each clause against s12BG (significant imbalance, not reasonably necessary, detriment if relied on) and the s12BH examples. Constraints: cite clause number. No customer identifiers. Output Format: a table with columns Clause number, Term summary, Limb 1 assessment, Limb 2 assessment, Limb 3 assessment, Overall (unfair / not unfair / requires legal review), Suggested rewording. Quality Bar: every Unfair finding must point to a s12BH example or a comparable analogue. Mark the output DRAFT FOR LEGAL REVIEW.

Prompt 3: Unconscionable conduct risk register entry

Role: Statutory unconscionable conduct analyst. Context: {{PRODUCT_OR_PROCESS}} targets a customer cohort with profile {{COHORT_PROFILE}}. Task: assess against the twelve s12CC factors and produce a risk register entry. Constraints: each factor scored High, Medium, or Low likelihood and impact. Cite Productivity Partners (HCA 2024) where relevant. Output Format: heat map plus a 200 word narrative summarising aggregate exposure and recommended controls. Quality Bar: scoring must be evidenced by reference to product, process, or customer characteristics. No anecdote.

Prompt 4: Plain English rewrite of disclosure paragraph

Role: Plain English editor for financial services disclosure. Context: paragraph {{PARAGRAPH_TEXT}} appears in a {{DOCUMENT_TYPE}}. Task: rewrite to a Flesch reading ease score of 60 to 70 while preserving every disclosure obligation. Constraints: no adjectives that imply endorsement or guarantee. No future-tense claims unless reasonable grounds exist. Output Format: rewritten paragraph plus a one-line note describing what was changed and why. Quality Bar: obligations preserved verbatim where verbatim language is required by the regulatory guide.

Prompt 5: Board paper executive summary on consumer protection exposure

Role: Compliance Officer drafting for a Risk Committee. Context: the attached pack covers consumer protection KRIs, recent reviews, customer remediation, and ASIC engagement. Task: produce a 250 word executive summary plus three recommendations. Constraints: plain English, Australian spelling, cite all materially negative findings. Output Format: heading, summary, three numbered recommendations with a named accountable owner. Quality Bar: every recommendation must be SMART and traceable to an underlying finding.

Prompt 6: Regulator response or s912D notification draft

Role: Compliance Officer drafting a response to ASIC under section 33 of the Act, or a s912D reportable situation notification. Context: the underlying matter relates to {{TOPIC}}. Task: draft a first-pass response. Constraints: cite the request, the controlling provisions, and any prior correspondence. No customer-level data. Output Format: response letter or notification with section headings matching the regulator's questions or the prescribed notification form. Quality Bar: every paragraph supports a named claim. No speculative content. Marked DRAFT FOR LEGAL REVIEW.

Governance, audit, privacy, and risk appetite controls

De-identification is mandatory. Real customer identifiers (name, customer number, account number, date of birth, address, contract reference numbers attributable to a person) must never be entered into a model prompt. Use stable pseudonyms and merge field placeholders. Where the analyst needs the link from pseudonym to underlying customer, that link is held outside the model context.

Human-in-the-loop checkpoints apply at every output stage. No PDS amendment, marketing piece, regulator response, contract reissue, or customer remediation letter is published or sent without a documented human review and senior manager sign-off. The model output is the draft, never the artefact.

Prohibited inputs include personally identifiable customer information, market-sensitive data, sanctions intelligence, claimant medical or financial vulnerability data, and any information subject to legal professional privilege the entity does not wish to risk waiving. Marketing claims carry a particularly high reputational tail; AI-generated marketing copy must clear an explicit second-line review before any external use.

Retention and logging: every model interaction relevant to consumer protection sign-off is logged through the Enterprise tenant logging facility, retained in line with the entity's evidentiary obligation to demonstrate reasonable basis under s12BB and ASIC's expectations under RG 78, and made available to internal audit on request. Model selection: Enterprise SaaS with no-training is the standard; on-prem or private cloud is required where the workflow handles customer-level data; public consumer-tier is prohibited. CPS 230: customer remediation processing and PDS approval are candidate critical operations under the entity's CPS 230 register and require documented disruption tolerance and operational resilience testing including failover to a non-AI workflow. APP alignment: APP 3 (collection), APP 6 (use and disclosure), and APP 11 (security) drive the prompt hygiene rules above; APP 1 governs disclosure of AI assistance to customers where appropriate.

Quality assurance loop

Run this five-step QA rubric against every AI output before it leaves the analyst's desk.

1. Source check. Every factual claim has a citable source. Every section, regulatory guide, or information sheet reference is correct.

2. Privacy check. No real customer identifiers, no third-party PII, no market-sensitive data.

3. Misleading conduct check. The output itself does not introduce a misleading impression. Disclaimers are prominent, clear, and not contradicted by the body of the document.

4. Material accuracy check. The output's central conclusion would survive an internal audit interview and an ASIC examination.

5. Evidence check. The output is annotated with the supporting evidence artefacts and would stand up at an ASIC investigation.

Red team prompt

Red team prompt to stress-test your own draft: "You are an ASIC enforcement lawyer reviewing this marketing piece, PDS section, or contract clause. Identify five reasons it could be misleading, deceptive, unconscionable, or unfair. Cite the section, regulatory guide, or case you are testing against. Score 1 to 10 on litigation risk. Recommend the smallest edits that would lift the score by 3 points."

Scaling pattern

Operationalise across the team as follows. First, codify each prompt as a versioned template in the project space (v1.0, v1.1) with a change log. Second, run a weekly evaluation cadence sampling outputs against the QA rubric. Third, set KRIs: percentage of PDS reviews requiring re-work after legal review, percentage of marketing claims requiring revision before sign-off, percentage of UCT scans surfacing previously unidentified clauses, and percentage of outputs failing the privacy or misleading conduct checks. Fourth, treat each model release as a change event: re-run the evaluation set and only promote at parity or better with a documented rollback path. Fifth, maintain a register of accepted and rejected use cases with rationale and review date. Sixth, publish an annual consumer protection AI assurance report to the Risk Committee.

Common Pitfalls and Watch-outs

Pitfall one on this list, treating a disclaimer as a cure for a misleading headline, is the most common and the easiest to test. Run every draft headline through this prominence check before it goes anywhere near a customer.

Six common failure modes recur in ASIC consumer protection enforcement and litigation. Each is followed by a one-line corrective action.

1. Treating disclaimers as a cure for a misleading headline. Courts repeatedly hold that a footnoted disclaimer cannot rescue conduct that is misleading at the level of overall impression. Corrective action: place qualifying conditions on the same screen, in equivalent prominence, as the headline rate or claim, and test the overall impression against the relevant class of consumers.

2. Forgetting that s12DA is fault-free. Marketing approvers sometimes argue the team did not intend to mislead. Intention is not an element of s12DA or s12DB. Corrective action: shift the internal challenge from "did we mean to" to "could a reasonable consumer in this segment be misled."

3. Approving standard form contracts without a structured s12BG assessment. The 2023 penalty regime makes this materially riskier. Corrective action: require every contract revision to be accompanied by a UCT review tracker showing each impugned-style clause assessed against the three-limb test.

4. Underestimating statutory unconscionable conduct exposure on vulnerable cohorts. Conduct that would not register as unconscionable for a sophisticated counterparty can readily be unconscionable for a customer with low literacy, language barrier, or financial stress. Corrective action: build a vulnerability lens into product approval and sales training.

5. Treating the s12DB representations as duplicative of s12DA. Each paragraph of s12DB(1) is a separate cause of action and now attracts its own civil penalty exposure. Corrective action: review draft material against each s12DB subsection individually, not as a single misleading conduct screen.

6. Failing to lodge a reportable situation under s912D where breach reporting timelines are engaged. The regime captures conduct that is likely to amount to a contravention of a financial services law. Corrective action: integrate the s912D self-assessment into the consumer protection remediation workflow rather than treating it as a separate, parallel process.

Decision Frameworks and Tools

The s12CC factor list is the operational checklist for statutory unconscionable conduct. This prompt turns it into a register entry your risk system can hold.

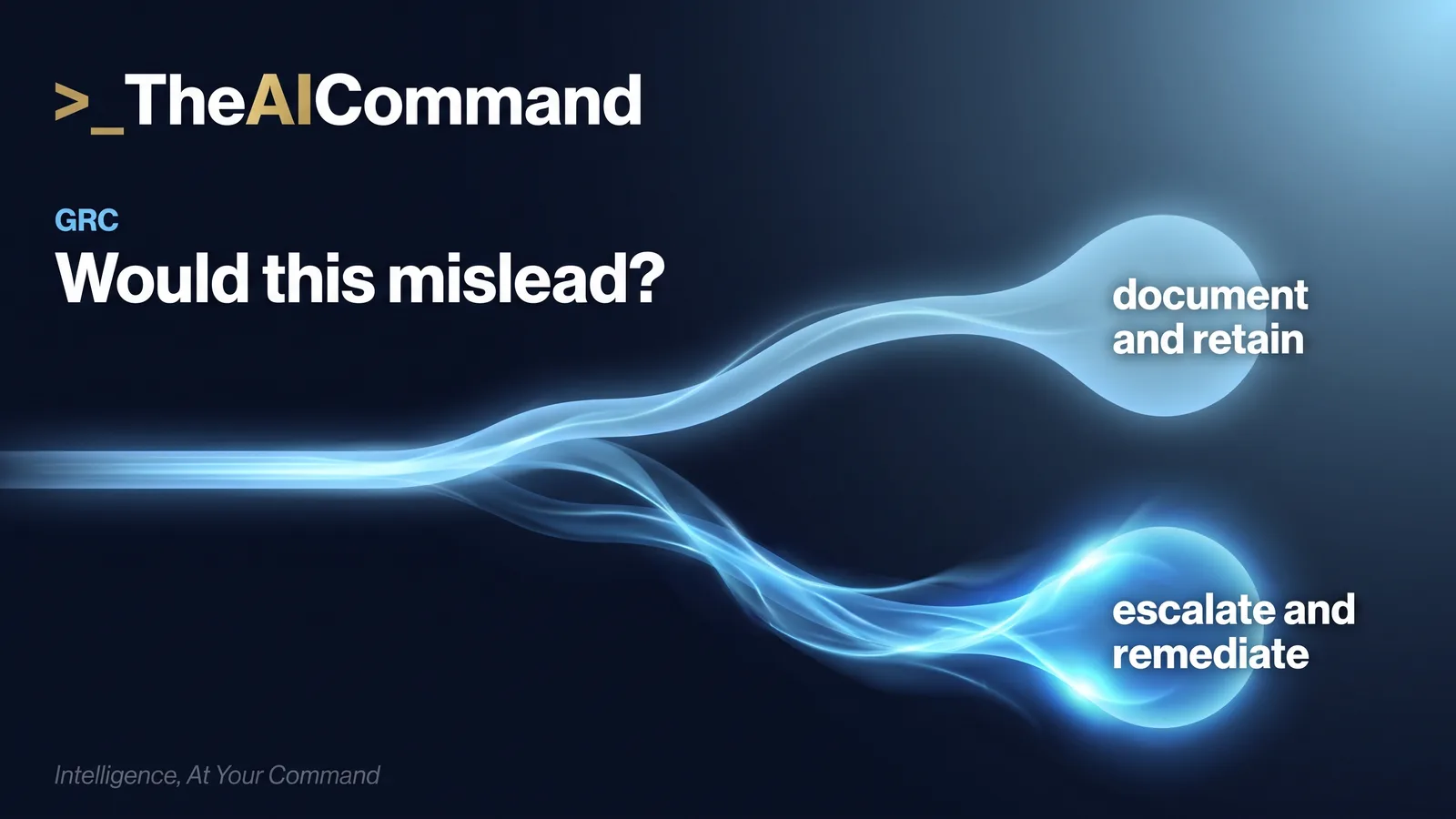

Decision tree: Is this conduct likely to mislead under s12DA?

Render as Mermaid for the designer.

flowchart TD

Q1[Conduct in trade or commerce in relation to financial services?] -- No --> Out[Outside s12DA. Other regimes may apply.]

Q1 -- Yes --> Q2[Identify the relevant class of consumers]

Q2 --> Q3{Would the conduct, taken as a whole including disclaimers, lead an ordinary or reasonable member of that class into error?}

Q3 -- No --> Doc[Document the assessment, retain marketing pack and approval log]

Q3 -- Yes --> Esc[Escalate to Legal and Compliance, halt distribution, draft remediation plan, assess s912D]

Esc --> Self[Self-report under s912D if reportable situation, log in the central register]

Maturity ladder for a consumer protection programme

Self-check questionnaire

1. Can I produce a current marketing approval policy and a UCT review register on request?

2. Can I trace any campaign or PDS to a documented s12DA / s12DB challenge before publication?

3. Have I run a structured s12CC factor assessment on every product targeted at a vulnerable cohort?

4. Have I rebased every standard form contract against the post-2023 unfair contract terms penalty regime?

5. Have I lodged a s912D notification on every reportable situation arising from a consumer protection breach in the last 12 months?

6. Is my AI-assisted consumer protection workflow logged, governed, and consistent with APP 3, APP 6, and APP 11?

7. Can my FAR-accountable Senior Manager describe the consumer protection control environment in their own words?

Further Reading and Authoritative Sources

Primary statute and rules

Australian Securities and Investments Commission Act 2001 (Cth), Division 2 of Part 2 (sections 12AA to 12HD). Corporations Act 2001 (Cth), section 1041H, Part 7.8A (Design and Distribution Obligations), and Part 7.9 (PDS regime). Competition and Consumer Act 2010 (Cth), Schedule 2 (Australian Consumer Law), sections 18, 20, 21, 22, and 23 to 28. Treasury Laws Amendment (More Competition, Better Prices) Act 2022 (Cth).

Regulator and government publications

ASIC, Regulatory Guide 234 Advertising financial products and advice services. ASIC, Regulatory Guide 168 Disclosure: Product Disclosure Statements (and other disclosure obligations). ASIC, Regulatory Guide 78 Breach reporting by AFS licensees and credit licensees. ASIC, Information Sheet 211 Clear, concise and effective disclosure obligations. ASIC, Report 762 Response to submissions on CP 354 (DDO). Treasury, Unfair contract terms reforms explanatory materials.

Case law

Productivity Partners Pty Ltd v ACCC [2024] HCA 27 (statutory unconscionable conduct). ACCC v Servcorp Ltd [2018] FCA 1044 (UCT). ASIC v Westpac Banking Corporation (BBSW) [2018] FCA 751. ASIC v MLC Nominees Pty Ltd [2020] FCA 1306 (misleading conduct in superannuation marketing).

Professional bodies

Governance Institute of Australia (Risk and Compliance Practice resources). Risk Management Institution of Australasia (RMIA) consumer protection papers. Australian Compliance Institute and the GRC Institute (formerly GRCI) practitioner resources. Financial Services Council guidance notes on disclosure and product governance.

Practical takeaways

Do this Monday

- Pull the current marketing approval policy and confirm it names s12DA and s12DB(1) challenge steps before external release. If it does not, log the gap with the policy owner today.

- List every live campaign headline claim and check that each qualification carries prominence equivalent to the claim it qualifies, applying RG 234.

- Ask contracts or product for the standard form contract register and confirm every template has a dated s12BG assessment completed after 9 November 2023.

- Identify the products targeted at, or likely to reach, vulnerable cohorts and confirm each has a documented s12CC factor assessment on file.

- Stand up the project space described in the AI operations section, load the Division 2 extract with RG 234, RG 168, and RG 78, and run the red team prompt against one live document.

The compliance checklist

- Division 2 of Part 2 (sections 12AA to 12HD) mapped to your product set, channels, and contract templates

- Marketing approval workflow with documented Legal and Compliance sign-off on every external claim

- Qualification prominence review against RG 234 recorded for every headline claim

- The ten s12DB(1) paragraphs treated as separate causes of action in the challenge template

- Standard form contract register with a current s12BG three-limb assessment for every template

- s12CC factor assessment on file for every product touching vulnerable cohorts

- Reportable situation analysis under s912D of the Corporations Act wired into the escalation path

- De-identification gate enforced before any document enters an AI workspace

- Human-in-the-loop sign-off recorded before any AI-assisted output is used externally

- Retention and logging of every AI interaction that informed a consumer protection decision

Your prompt library

The four prompt boxes in this module cover the misleading conduct red team, the unfair contract terms scan, the s12CC factor walkthrough, and the qualification prominence check. Save them as versioned team assets in your project space and pair each with the five-step QA rubric from the AI operations section. When you need a fast, board-ready readout, the bonus prompt below condenses the whole assessment into a five-minute pass.